Demystifying the MBCBP

In this article I will explain…

-

What a cash balance plan is in simple terms.

-

Details on how cash balance plans are structured.

-

Why a defined contribution with cash over cap is NOT better.

On July 20, 2023 I published a post correcting some of the details in this article. Read it here.

Last Monday I was minding my own business golfing with colleagues before a conference when my phone started blowing up. I quickly found out that the long awaited and soon to be passionately argued Tentative Agreement was here! It was like Christmas morning if the thing you love most is reading contract language. Incidentally that is NOT the thing I love most, but I still dove in to find out what the new retirement package will look like if this TA passes.

Unsurprisingly, the answer to “what kind of retirement plan structure will replace the traditional Final Average Earnings A plan” is a cash balance plan. Cash balance plans are an increasingly popular plan design in retirement planning, especially as an alternative to a traditional defined benefit pension plan. This is certainly not a new or novel type of plan. After all, there are only two types of defined benefit plan structures available, and the cash balance plan is much easier to administer.

There seems to be a lot of confusion about what this cash balance plan is, and more importantly if it’s the best alternative for the traditional defined benefit plan. The mechanics of this plan are not hidden or abstruse. It’s actually quite simple!

In this post, I hope to demystify how these plans are structured and dispel some troubling myths that I’ve heard. As an independent financial advisor, I am an outside observer with education and experience with these plans. My goal is to arm FedEx pilots with the information necessary to make informed decisions. I do not have an opinion on how anyone should vote, nor specific advice on whether this new plan is right for your personal situation. What I hope you gain from reading this is a full understanding of what this plan is, how to compare it to what it’s replacing and how it stacks up to other alternatives that have been discussed.

What is a cash balance plan?

In the most simplistic terms, here is how a cash balance plan works. Each participant gets a hypothetical account. Each plan year, the company increases balance via a contribution to your account. They take the money they contribute across all participants, lump it together, and throw it into a bucket (the trust). They hire professionals to invest the money that is in the trust. Each plan year, they also decide on an interest credit that is calculated on your hypothetical balance and added to your balance. The result is each year your account balance (cash balance) stair steps up based on contributions made and interest credited. When it’s time to take distributions, you can roll the accrued balance into an IRA, or choose to receive a monthly income like the A plan you are used to. That’s it! At their core, these plans are no more complicated than that!

Ok, I’m ready for more details…

Let’s start with the interest crediting rate. Traditionally, cash balance plans feature a fixed interest rate, though some - including the new MBCBP for FedEx pilots - feature a variable interest rate. This variable rate gives the ability for the participant to have share in the investment returns on plan assets. Importantly, by law this interest rate CANNOT be negative.

When a company elects a fixed rate, it is set low enough to be easy to achieve and exceed on a consistent basis. For instance, the fixed interest rate on the cash balance plan available to non-pilot FedEx employees is 4%. The company bears all investment risk, the participant earns 4% per year, and the plan keeps all investment returns above 4%. With a variable rate, the company still bears all the investment risk, but they along with their advisors (investment professionals, ALPA oversight, etc.) can raise or lower the credited interest rate based on the actual performance of the plan assets. This is done specifically so that participants share in excess investment returns. The company cannot make any of these decisions on a whim. The process used to determine the asset allocation and interest crediting rate is governed by the Investment Policy Statement (IPS). ALPA has been given an advisory role on the IPS so they will have input, but the company is the fiduciary. This means that they are obligated to adhere to the IPS, and they alone will be held legally responsible if they do not.

The way contributions are calculated makes the plan look like a defined contribution plan (since the contributions are defined in advance), but it’s important to understand that a cash balance plan is a type of defined benefit plan. This means that the limits are defined on the back end by the income benefit it can provide at retirement, rather than on the front end by the contributions that go in. This is a very important distinction that in practice can potentially enable an unparalleled amount of future additional access to tax deferral in retirement. That’s because these plans are not subject to the IRC § 415(c) limit ($66,000 for a 401(k) in 2023). In fact, there is no published annual contribution limit for a cash balance plan. Instead, they are subject to a maximum pension benefit limit, the IRC § 415(b) limit ($265,000 in 2023). This means that the participant’s balance is limited to the amount that would actuarially pay a $265,000 benefit (approximately $3.4 million). Annually, the contributions do have a reachable limit, but that limit is actuarially calculated based on the maximum benefit, so it is different depending on age, but generally the limit is into the hundreds of thousands of dollars. You would have to be receiving contributions of 50% of pay or higher in order to get close to these limits. One additional limit to be aware of is the IRC § 401(a)(17) limit. This limit governs the compensation on which contributions can be based. By law, no compensation above this limit ($330,000 in 2023) can be considered in contribution formulas in qualified retirement plans.

Contrary to what some have stated, the costs to administer a cash balance plan, especially one the size of FedEx, are not materially different from the traditional defined benefit pension plan. There are actuarial costs associated with both. For a company the size of FedEx, the costs are negligible compared to the size of the benefit.

The real cost difference is when there are increases in the plan. In a traditional defined benefit pension plan, future increases to the benefit increase both future and past benefit accruals. This raises the cost of increasing benefits in a traditional defined benefit plan substantially, making it much harder to negotiate increases to the Final Average Earnings formula. In a cash balance plan, future benefit increases raise the cost of funding future accruals, but not past accruals. While this is not a benefit for the participant, it does potentially make it easier to negotiate future increases, and as mentioned above, there is PLENTY of room for future increases.

I don’t trust the company to invest my money, so why can’t I as the participant have control over where my money is invested?

The company MUST be the sole fiduciary on the account. There is no legal alternative to this structure. As sole fiduciary the company is legally bound to act in the participants’ best interest, rather than their own. They are held to this standard when making asset allocation decisions and choosing the interest crediting rate in accordance with plan documents and the IPS. Additionally, they are responsible for funding benefit shortfalls just like any other defined benefit plan. Choosing to arbitrarily reduce the interest rate below what is set out in the IPS would be a breach of fiduciary duty for which they would be held liable. There is no upside for them to do this. Because plan assets are held in trust, keeping large excesses in the plan by unnecessarily reducing the interest crediting rate does nothing for them. It wouldn’t change how much they must contribute, and they can’t get it back once it’s in there.

Additionally, a participant cannot control the assets in their account because a participant account is only hypothetical. There are no separate accounts. Plan assets MUST be invested together for the benefit of all participants, so there is no way to segregate one participant’s balance from the others to self-direct until the participant takes a distribution, whether in-service or at retirement.

Not only can there just be one fiduciary structurally, the plan sponsor MUST be that sole fiduciary. This point cannot be reiterated enough. This is mandated by IRS regulation! It is non-negotiable! Even if it was negotiable, it would be foolish for participants to take on that responsibility in the plan. FedEx, as sole fiduciary, will as part of their investment process hire a large institutional investment firm consisting of professional investors and allocators. There will be teams of CFAs allocating the funds, and other teams of CFAs providing oversight. The fiduciary bears the risk of loss in plan assets, but a participant’s hypothetical account does not. If the pilots (ALPA) were able to take on that fiduciary role, I would hope that the investment process would be the same. And what IF (big if) things go south such that there would be a lawsuit for breach of fiduciary duty? Who would participants sue, themselves? ALPA has already been given oversight opportunity in the new deal. They can monitor and audit the plan in relation to the IPS, but they are NOT a fiduciary of the plan. There is no other way to do it, but even if there was, this structure would make the most sense for pilots.

So then why not cash over cap?

Some have said that a straight defined compensation contribution into the 401(k) with “cash over cap” is a better solution for one reason or another. Because the 401(k) is a defined contribution plan, it is subject to the §415(c) limit ($66,000 in 2023) on total contributions from all sources (excluding catch-up contributions). This is what is referred to as the “cap”. Hence the cash over cap provision, which would direct non-elective contributions in excess of the §415(c) limit to the pilot as compensation. Assume a pilot makes at or above the IRS compensation limit for contributions, which is $330,000 in 2023. Let’s assume the pilot makes personal contributions up to the 2023 limit of $22,500. After the $500 match, a new 20% contribution of $66,000 would force $23,000 in cash over the cap. Unless this money had somewhere else to go (hint: a cash balance plan is the only possible place, and only if the plan sponsor allows), it would have to hit your income taxes in the year received before it could be invested anywhere. This is a massive inefficiency that would be silly to ask for.

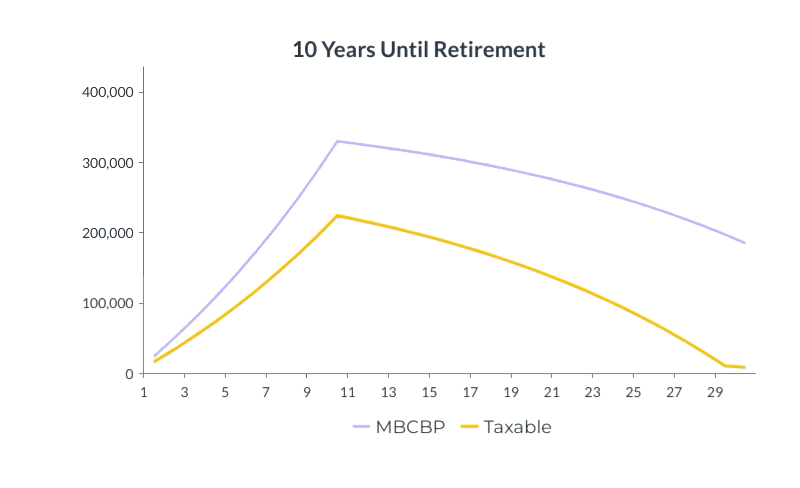

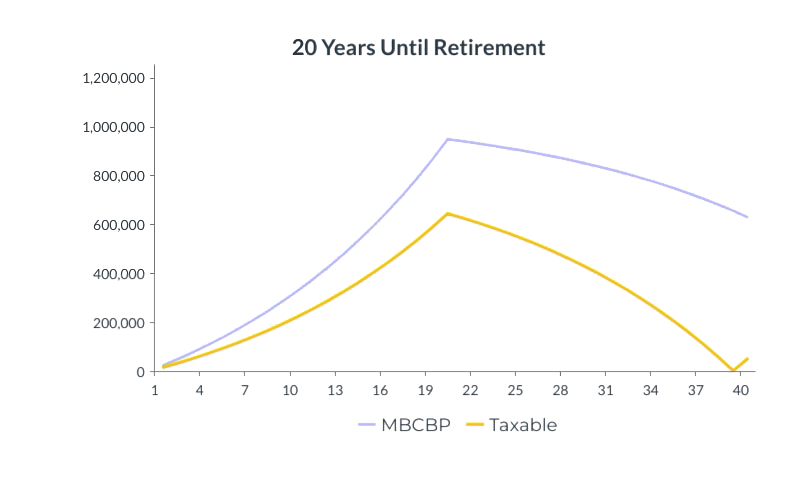

Look at the two graphs below. In these examples, I isolated the inefficiency of the cash received over the cap being invested in a taxable account.

In both examples, I assume that the pre-retirement top tax bracket is 32%, the post-retirement top tax bracket is 24%, and the capital gains rate is 20%. I assume a 6.5% return on cash balance plan assets and a 6.5% return on assets in the taxable account. To simplify things, I assume that capital gains taxes are the only taxes associated with the taxable account (unlikely) and that all taxes on gains are deferred until sale of assets for income (also unlikely).

Example 1 is a 10-year time horizon until retirement.

After benefits accumulate for 10 years, the amount accrued in the taxable account can distribute a net income of $18,000 for 20 years before it runs out of money. Distributing the same net income from the MBCBP leaves almost $200,000 in the account still after 20 years! Modeling the max income from the MBCBP over 20 years yields 16% additional income annually!

Example 2 is a 20-year time horizon.

When the accumulation period is 20 years, the difference is even larger. The taxable account can provide $50,000 in net income before it is exhausted. The same net income from the MBCBP leaves over $600,000 left in the MBCBP after 20 years. Modeling the max income from the MBCBP in this scenario yields 19% additional income annually!

It should be clear from these examples that cash over cap in the 401(k) plan (absent a spillover to a cash balance plan) is way worse for almost everyone. The only people this would benefit are people who get paid a percentage to invest your assets.

I’ve heard from some of my clients that this plan has been described as a “Tax Ticking Time Bomb™️”. I’m not sure where this is coming from, but I’ve heard the phrase my entire career. It usually accompanies a total lack of understanding of tax planning in real world retirement distribution planning. That, or a sales pitch for a product that features a great commission for a salesperson.

The Tax Ticking Time Bomb™️ scare tactic is used to describe the income taxes that are due on distributions from retirement plans that have not been taxed yet. The idea is that if you have a substantial portion of assets tied up in accounts that are taxed at income rates when you take distributions in retirement, and your income in retirement is high enough to still be in a high tax bracket, you will pay a bunch in taxes when you take those distributions. Makes sense. That would be a problem if there was some other plan structure that avoided this. There isn’t!

Like it or not, as a W-2 earner there is no avoiding income taxes. With the narrow exception of an HSA used for medical expenses, your money either gets taxed on the way into the account, taxed on the way out, or both. Tax diversification is something everyone should be thinking about, and it is something we work on diligently with clients. There are ways to address this like Roth and after-tax contributions, Roth conversions, and other things that give you more control over your tax bracket in retirement. But the company does not make Roth contributions on your behalf, so this can’t be done by a different plan structure like cash over cap. In fact, a cash over cap plan structure would impinge on your ability to solve tax diversification by crowding out opportunities to make after-tax contributions!

Which plan is right for me?

This is a very personal question, and one that you should certainly consult a CFP© professional to answer. Your situation will have a unique set of circumstances that may sway you one way or the other. Generally, the shorter your time horizon to retirement, the better the traditional plan would be for you, but where that crossover line is dependent on many personal factors. The modeler is a great place to start, but there is no one-size-fits-all rule of thumb. If you are curious about how this new plan would affect your personal situation, schedule a free consultation meeting with us today.

But one thing is clear to me. As someone who is familiar and has experience with all of the types of qualified and non-qualified retirement plans, this plan is a well-designed alternative to the A plan. You could argue about whether the contributions are big enough to warrant you choosing it. But there is no other plan design that combines the security, efficiency, and growth potential of the MBCBP.

Nathan Harro is a CFP© professional and the founder of Centennial Wealth Group, a full-service financial planning and wealth management firm that specializes in working exclusively with FedEx pilots. For more information on this or other financial planning needs, schedule a call with us!

All information presented is collected from sources believed to be reliable, but may not be guaranteed. It is meant to provide general education and should not be considered or a recommendation to take a particular course of action. The hypothetical examples are for illustrative purposes only and should not be construed as a prediction or guarantee of actual results.